A Revolution in Energy Storage

A Gravity Power plant is simple, reliable, and elegant. We dig a deep shaft, using standard technology from the mining industry. We build a piston of reinforced rock in the shaft. We add water and cap it, creating a closed loop system, with no additional water required.

A conventional pump/turbine forces water down the penstock into the shaft, lifting the piston. With highly efficient hydropower equipment and low piston speed, system efficiency is high. Thousands of megawatt-hours can be stored in each plant.

As the piston drops, it forces water up the penstock and through the turbine, spinning the generator to produce electricity.

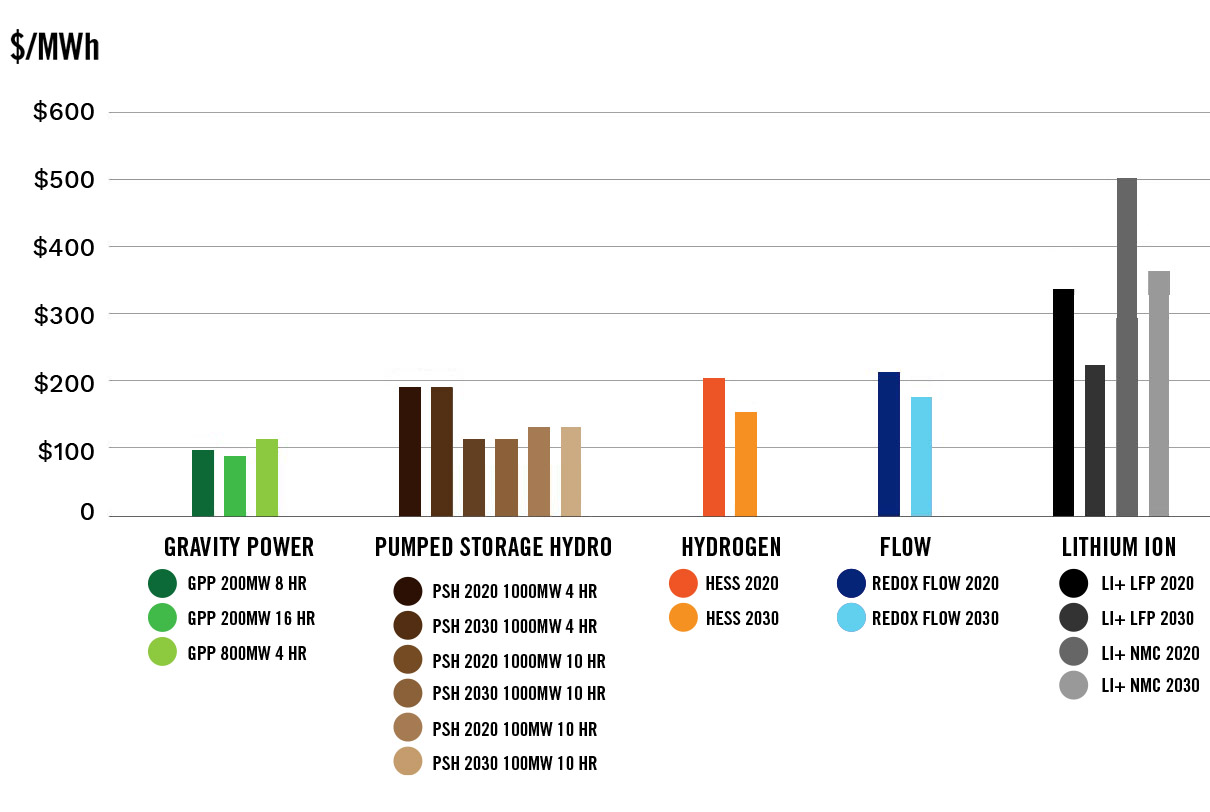

(Data for PSH, H, Flow, Li+ from Pacific Northwest National Lab. Data for GP from management.)

© Crossrail Ltd 2021

Denis Egan, CC BY 2.0, via Wikimedia Commons

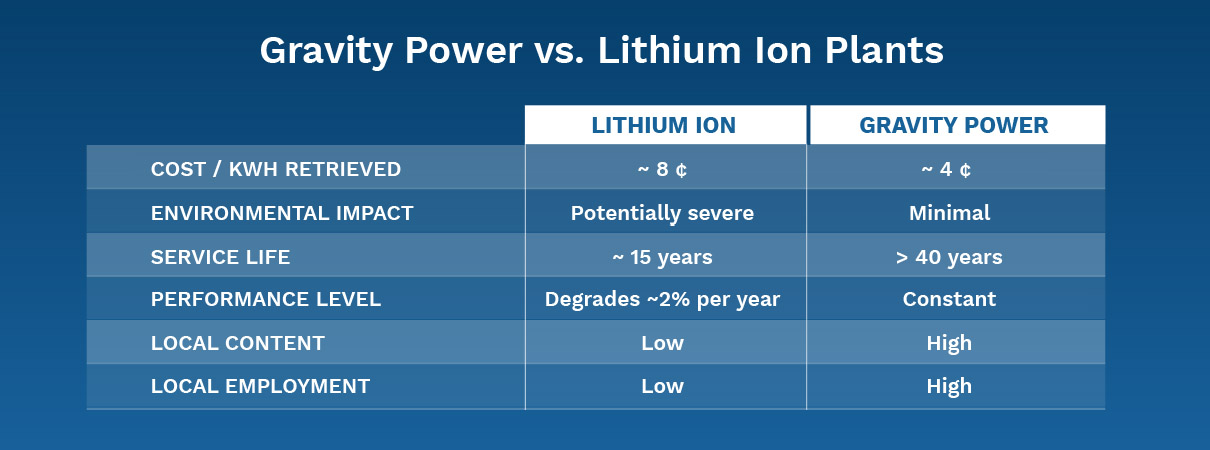

Gravity Power provides scalable, cost-effective, highly efficient energy storage, using existing commercial technologies, without the environmental and technical difficulties of pumped storage hydro, batteries, or other solutions.

Gravity Power will revolutionize the $1+ trillion market for energy storage. Energy is stored when the pump drives water down a deep underground shaft, raising a piston. To return energy to the grid, the piston descends with gravity, driving water through the generator. Our facilities can be built in a wide range of locations: at renewable power plants, on brownfield sites, even in cities.

Gravity Power has built a strong leadership team and advisory board, including globally recognized experts in energy markets, regulatory policies, control theory, system analysis, generation scheduling and control, power grid control, hydroelectric systems engineering, underground engineering and construction, and sealing technologies.

Tom Mason and Jim Fiske also serve on the Board. Recruitment is underway for additional Directors.

EPC Partner: Underground Engineering and Construction

Leading company worldwide specializing in underground engineering. Has supported more than 200 tunnelling projects worldwide. Core area of expertise in mechanized tunneling with tunnel boring machines. Further focus are special projects requiring customized solutions and trouble shooting for TBMs in difficult situations. Spun off Tunnelsoft with TPC (Tunneling Process Control), an encompassing software to manage all tunneling related data and to allow efficient visualization and automated data evaluation.

Supplier & Seal Expertise

Leading specialist worldwide in sealing applications, serving customers in a wide variety of industries. Combines longstanding engineering and market know-how with unique material expertise. Focused is on serving our customers’ most progressive (or cutting-edge) industrial opportunities and needs. The company also works collaboratively with customers on the design and validation of custom sealing systems.

As utilities deploy more renewable energy, Gravity Power can offer a storage solution that protects the environment, lowers cost for ratepayers, and provides local jobs.

Renewable energy producers require storage to maximize market share and profitability. Most producers are moving away from chemical-based storage technologies, because of cost and environmental impacts.

Builders are essential to our next-generation storage solutions. Gravity Power Plants provide a pathway to more projects, more revenue, and more contributions to their regional economies.

Local, state, and national governments need to set energy policies to achieve a carbon-free energy sector. We provide a path for this, while protecting the environment, keeping consumer costs low, and providing local jobs.